Negotiated Rebates on Generics: What Insurance Actually Pays

When you fill a prescription for a generic drug like metformin or lisinopril, you might assume the insurance company pays a small, straightforward amount. But here’s the truth: what insurance actually pays for generics isn’t what you see on the receipt. It’s hidden behind layers of contracts, secret fees, and financial maneuvers that rarely involve rebates at all.

Generics Don’t Work Like Brand Drugs

Brand-name drugs often come with big rebates - sometimes 50% or more of the list price. These rebates are negotiated by pharmacy benefit managers (PBMs) in exchange for putting the drug on a preferred list. The insurer pays the full list price upfront, then gets money back later. But generics? They don’t play that game.Why? Because generics are already cheap. There are 10, 20, even 50 manufacturers making the same pill. Competition drives prices down. No single company has enough power to demand a rebate. Instead of rebates, the system uses something else: spread pricing.

Spread Pricing: The Hidden Cost

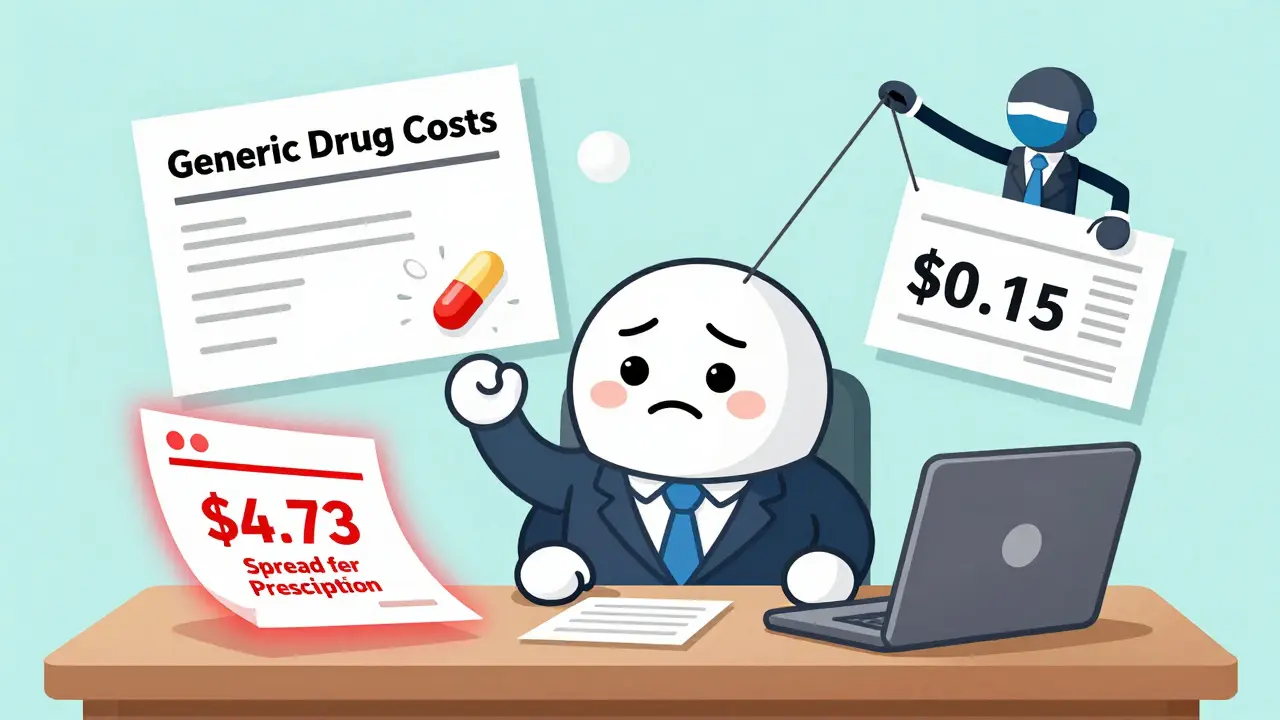

Here’s how spread pricing works. Your insurer thinks it’s paying $8.50 for a 30-day supply of generic atorvastatin. The pharmacy gets paid $4.25. The difference - $4.25 - goes straight into the PBM’s pocket. That’s not a rebate. That’s profit. And you won’t find it on your explanation of benefits.The Department of Health and Human Services found in 2022 that the average spread on generic prescriptions was $4.73 per drug. Multiply that by millions of prescriptions, and you’re looking at billions in hidden fees. Employers with self-funded plans often don’t realize they’re paying this until they audit their PBM contracts. One Fortune 500 HR director told Becker’s Hospital Review they discovered their PBM was keeping $4.25 per generic prescription - and had never disclosed it.

Why Don’t PBMs Just Use Rebates on Generics?

It’s not that PBMs can’t negotiate rebates on generics - it’s that they don’t want to. Why? Because rebates are small. A 2-5% rebate on a $1 pill doesn’t move the needle. But a $4 spread on that same pill? That’s a 400% profit margin.Rightway Healthcare’s 2023 report shows PBMs often favor brand-name drugs over generics, not because they’re better, but because they bring in bigger rebates. A PBM might exclude a $0.15 generic in favor of a $5 brand-name drug with a 60% rebate. The insurer pays more upfront, gets a rebate back, and thinks it saved money. But the patient still pays more out-of-pocket, and the total cost is higher.

What Insurance Actually Pays: The Real Math

Let’s break it down with real numbers:- List price of generic: $10

- Pharmacy cost (what the pharmacy pays the wholesaler): $4

- Insurer pays pharmacy: $8.50

- PBM keeps: $4.50

- Net cost to insurer: $4 (after accounting for the spread)

So, while the insurer writes a check for $8.50, its actual cost is closer to $4 - but only if the PBM passes along the true cost. Most don’t. That’s why 68% of large employers in a 2023 survey couldn’t figure out what they were really paying for generics.

How This Affects You

If you’re on a high-deductible plan, you pay the $8.50 at the pharmacy. If you’re on a low-deductible plan, your insurer pays it - but you still pay higher premiums because the insurer’s costs are inflated by spreads. Either way, you’re paying more than you should.And here’s the kicker: the system discourages generic use. If a PBM makes more money from a brand-name drug with a rebate, it may block the generic from your formulary. You might need a prior authorization, or your doctor might not even know the cheaper option exists.

What’s Changing?

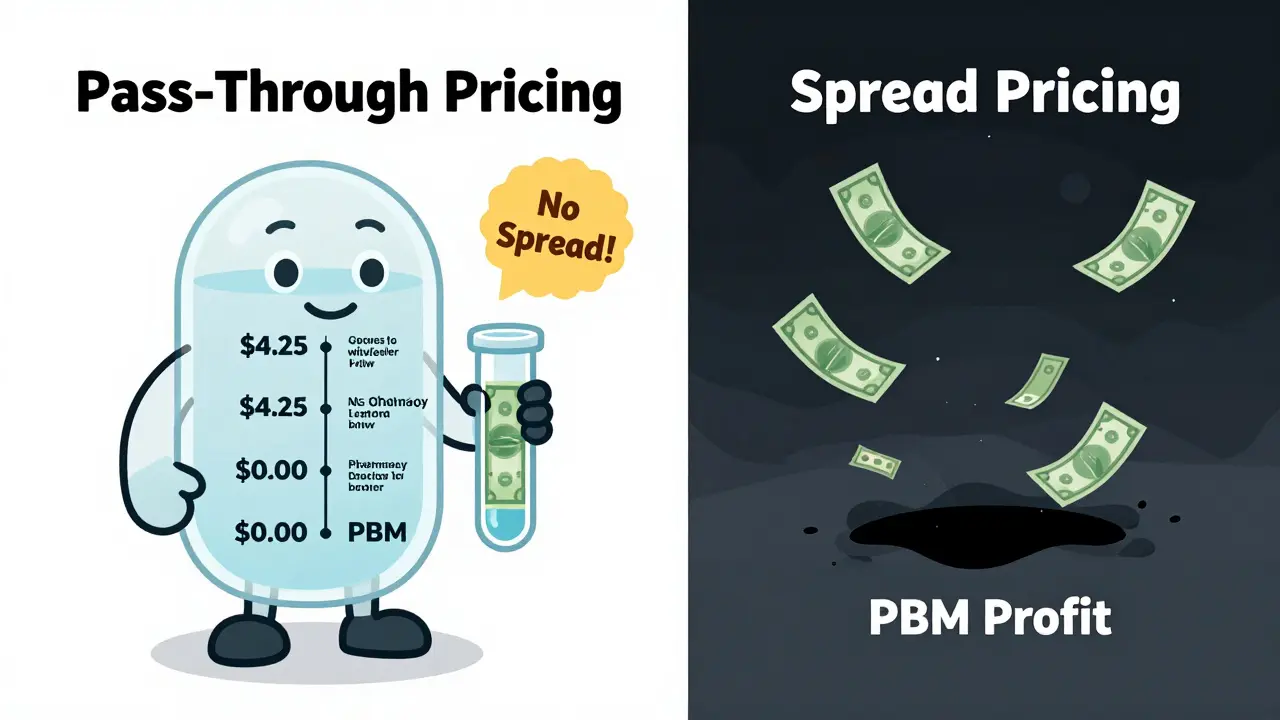

The tide is turning. The No Surprises Act of 2020 forced some transparency, but it didn’t go far enough. Now, 42% of large employers have switched to pass-through pricing - where the PBM charges a flat fee instead of taking a spread. That means you pay the real cost: what the pharmacy paid for the drug, plus a transparent admin fee.According to the National Business Group on Health, that number jumped from 18% in 2020 to 42% in 2024. The Employee Benefit Research Institute predicts full disclosure of generic acquisition costs will be required by 2026. The Congressional Budget Office estimates eliminating spread pricing could save employer plans $5-7 billion a year by 2027.

What You Can Do

If you’re an employee: ask your HR department if your plan uses pass-through pricing. If you’re a small business owner: demand it. If you’re a patient: ask your pharmacist what the generic actually costs. You might be surprised.Generic drugs make up 90% of prescriptions in the U.S. but only 23% of spending. That’s the power of competition - if the system worked the way it should. Right now, it doesn’t. The money’s being hidden where no one’s looking.

What’s Next?

The Biden administration’s 2024 executive order is pushing HHS to examine practices that limit generic use. CMS has started negotiating prices for brand-name drugs under the Inflation Reduction Act - but generics are explicitly excluded because, as the law says, they’re already competitive.That’s the irony: the system that should be saving you money is the one making it harder to save.

Do generic drugs ever have rebates?

Rarely, and if they do, the rebates are tiny - usually 2% to 5% of the list price. That’s because generic manufacturers compete on price, not rebates. Most savings come from low wholesale costs, not post-sale discounts. PBMs rarely negotiate rebates on generics because the financial upside is too small compared to the profit from spread pricing.

Why does my insurance pay more for a generic than what the pharmacy pays?

Because your PBM is using spread pricing. They tell your insurer they’re paying $8.50 for a drug, but they only pay the pharmacy $4. The $4.50 difference goes to the PBM. This isn’t a rebate - it’s a hidden fee. Many insurers don’t even know this is happening until they audit their contracts.

Can PBMs block generic drugs to favor brand-name ones?

Yes. PBMs often design formularies to prioritize brand-name drugs that offer large rebates - even if a cheaper generic exists. A PBM might exclude a $0.15 generic because it doesn’t generate a rebate, and instead include a $5 brand-name drug with a 60% rebate. The insurer thinks it saved money, but the patient pays more out-of-pocket, and the total cost goes up.

Is there a difference between what a generic drug costs and what insurers pay?

There’s a huge difference. The actual cost - what the pharmacy pays the wholesaler - is often under $5 for a 30-day supply. But insurers are billed $8-$12. That gap isn’t inflation. It’s spread pricing. The PBM pockets the difference. Without transparency, insurers think they’re paying more than they are - and patients pay the price in higher premiums and deductibles.

What’s the best way to know what my insurance really pays for generics?

Ask your employer or insurer if they use pass-through pricing. In this model, the PBM charges a fixed administrative fee (like $2 per claim) and passes along the true cost of the drug. You’ll see exactly what the pharmacy paid, plus the fee. If they use spread pricing, demand a contract audit. You have the right to know how your drug dollars are being spent.

14 Comments

This is the exact reason I stopped trusting my insurer. I pay $15 for metformin at the pharmacy, but my employer's audit showed the PBM was charging $11.50 and pocketing the rest. No rebates. Just pure spread pricing. And we're all paying for it in higher premiums.

It is imperative that we, as informed consumers, demand full transparency from our pharmacy benefit managers. The current system is not only ethically dubious but also economically unsustainable. Employers must insist on pass-through pricing models to ensure fiduciary responsibility and equitable cost distribution.

I had no idea this was happening 😡 Seriously, I thought generics were supposed to be the affordable option. Now I’m realizing my $4 copay is actually subsidizing some PBM’s luxury vacation. This needs to be曝光ed everywhere. #HealthcareFraud

Of course they do this. The whole system is rigged. You think Big Pharma is the villain? Nah. It’s the middlemen. The PBMs. The guys who don’t make a single pill but somehow own your prescription. Welcome to America.

I’ve been pushing my company to switch to pass-through pricing for two years. Finally got them to audit last quarter. We were overpaying by $1.2 million annually on generics alone. Simple fix: stop letting PBMs hide the math.

I’m sorry, but this article is just… overly dramatic. You’re acting like this is some new scandal. This has been common knowledge in healthcare administration since 2015. Everyone who works in benefits knows this. You just didn’t read the fine print.

In India, generic drugs are sold at near-wholesale prices because there’s no PBM layer. Pharmacies buy directly from manufacturers. The system works because there’s no middleman profiting from opacity. Maybe we should look at models outside the U.S. instead of just complaining about it.

I used to work at a PBM. We called it ‘spread’ but everyone knew it was just skimming. We didn’t even bother hiding it from clients-most didn’t care as long as the premium didn’t jump. It’s not evil, it’s just… capitalism. 😅

The real tragedy isn’t the spread pricing-it’s that we’ve normalized it. We accept that a $0.15 pill costs $8.50 because we’ve been trained to believe ‘insurance’ means ‘protection.’ But it’s not protection. It’s a performance art of financial obfuscation. And we’re all actors.

The data from the HHS report is clear: the average spread on generics was $4.73 per claim in 2022. With over 4 billion generic prescriptions filled annually, that’s $18.9 billion in hidden fees. The Congressional Budget Office’s estimate of $5–7 billion in annual savings from eliminating spreads is conservative. This is not theoretical-it’s measurable, quantifiable, and preventable.

Oh wow, a 400% profit margin? How shocking. I guess the PBM CEO just woke up and said, ‘Hmm, what if we charged people for the air they breathe?’ Genius. Truly. I’ll be sure to send my resume.

The PBM ecosystem is a parasitic value chain. It thrives on information asymmetry, regulatory capture, and the false narrative of ‘cost containment.’ The structural incentives are designed to maximize margin, not patient outcomes. This isn’t market efficiency-it’s institutionalized extraction. The only solution is structural reform: nationalized acquisition pricing or public PBM.

Just ask your pharmacist what the drug actually costs. They’ll tell you. Then ask your HR if your plan uses pass-through pricing. If they don’t know, you’re being screwed.

I work in pharmacy and see this every day. We get paid $3.80 for a 30-day of lisinopril. Patient pays $10. Insurer gets billed $9.20. We’re not making bank. The PBM is. And yeah, they’ll block the generic if a brand has a rebate. It’s wild. But I’m glad more people are starting to notice.